|

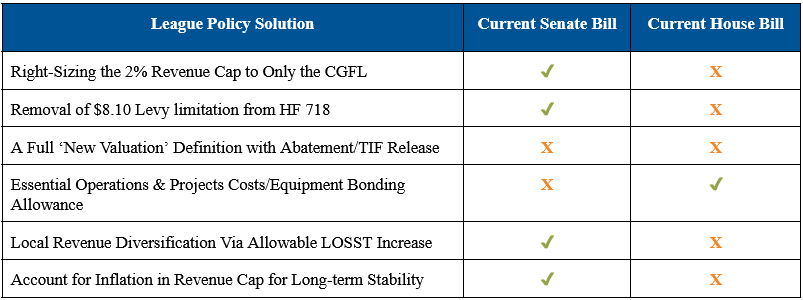

It is vital local officials continue to engage with their state legislators to present the policy solutions developed by the League, which can be accessed in the League’s Legislative Toolkit. Some of these policy solutions are included in each current proposal as displayed in the chart above. The League recognizes that both bills under consideration will impact local government service funding, however, without including these policy solutions in a final property tax bill, cities will not be able to sustain the property tax relief the legislature and local officials are looking to deliver for taxpayers.

These conversations matter. Lawmakers need to understand that while property tax relief is a shared goal among state and local officials, it comes with real trade-offs. Your real-world, on-the-ground perspective is critical to ensuring they have a full picture before they cast a vote.

Just as important: report back. After connecting with your lawmakers, please share what you’re hearing with the League. Your notes on their feedback is essential as we continue to engage at the Capitol on behalf of Iowa’s local communities.

The League will continue to advocate alongside partner organizations for the inclusion of these policy solutions in each property tax proposal as well as the other provisions in each bill which impact local governments. As an update to this week’s property tax developments at the Capitol, Piper Sandler & Co. is working to model the newly amended legislation. The League will be pulling down the current outdated models until updated versions may be completed.

House Property Tax Proposal Summary | HF 2745

-

Retains a hard 2% revenue cap on all levies outside debt service

-

Retains releases from Abatement in the definition of New Valuation exempt from the 2% cap

-

Requires cities establish an “obligated funds account” which will hold any funds that are being saved for large equipment purchases/maintenance of horizontal/vertical infrastructure

-

Adopts League policy solution to allow for essential operations costs for infrastructure/capital improvement projects and large equipment

-

Adds an additional Homestead Exemption of $15k on top of the rollback

-

Includes League’s improved taxpayer notice language

-

Lowers school foundation levy from $5.40 to $4.90

-

Removes increase of the Business Property Tax Exemption from $150k to $350k

-

TIF Provisions:

-

Repeals Section 403.22 relating to LMI

-

Takes the school foundation levy out of future TIF agreement diversion

-

Takes voluntary EMS levies out of TIF diversion immediately upon enactment

-

For Perpetual TIFs:

-

20 years after the effective date a city is limited to receive a max of 60% of the TIF increment generated. Any amount above 60% must be allocated to the other taxing entities

-

Future TIF agreements limited to 23 years

-

Adds the ability of a school district to opt-in all or a portion of the school foundation levy if approved by resolution

Sidewalk Liability | SF 2146 & HF 2359

The League’s sidewalk liability priority bill has a technical amendment which would realign sidewalk liability to the adjacent property owner for future claims. Conversations continue with House leadership to move the bill to the floor for debate. The legislation has already been passed by the Senate. |